Assistant Review Director and CPA Reviewer, CPA Review School of the Philippines Special Lecturer, Accountancy Department, Philippine School of Business Administration Manila Graduate Student, MBA in Technology and Entrepreneurship, La Consolacion College Manila

Abstract

Applying Philippine Financial Reporting Standard (PFRS) 15 presents several challenges, including limited testing on whether Artificial Intelligence (AI) improves its implementation, a lack of Philippine data on PFRS 15 complexity, and the absence of variables linking AI and PFRS 15. This study evaluated whether respondents from selected Philippine auditing firms perceive AI as a valuable strategic resource in implementing PFRS 15. The study calculated the mean, standard deviation, and variance of survey responses and used PLS-SEM to explain The relationships between AI-related and PFRS 15-related variables. Findings showed that respondents perceived low adoption of AI for PFRS 15 applications, but those with AI experience reported that it was highly effective and that accuracy closely aligned with this effectiveness. The study recommended that auditing firms invest in staff training and AI technologies to enhance the implementation of PFRS 15.

Keywords: Philippine Financial Reporting Standard (PFRS) 15, Artificial Intelligence (AI) -Driven Systems on Revenue Recognition, Financial Reporting Accuracy, Data Validation, Predictive Analytics, Mitigating Risks

Introduction

Income is an increase in assets or a decrease in liabilities, resulting in increased equity, except for owner contributions or investments (IFRS 15, 2018). Income may take the form of revenue—income from a company’s primary activities. Recognizing revenue is essential to financial reporting, as it reflects a company’s financial performance. To guide this, the International Accounting Standards Board (IASB) issued IFRS 15: Revenue from Contracts with Customers in May 2014. It became effective for accounting periods beginning January 1, 2018. The Financial and Sustainability Reporting Standards Council (FSRSC) adopted this as the Philippine Financial Reporting Standard (PFRS) 15. Revenue recognition follows five steps: contract identification, identification of performance obligations, determination of the transaction price, allocation of the price to each obligation, and revenue recognition.

Implementing PFRS 15 reveals several challenges (Osma, Conde & Mora, 2023), including high implementation costs, complexity, resistance to change, and information disclosure requirements. These challenges necessitate that companies upgrade their information technology systems, and, due to the complex requirements of PFRS 15, the timing of revenue recognition may be delayed. In a study conducted in Cagayan (Manuel et al., 2019), difficulty in adopting the five-step model had the highest frequency (30.43%).

Companies use Artificial Intelligence (AI) to increase operational productivity (Cardillo, 2025), and a 2024 McKinsey and Company survey found that 50% to 72% of businesses used AI in their operations. A 2023 survey by Forbes Advisor found that 30% of business owners use AI in their accounting processes, and the majority believe AI will have a positive impact on their businesses. Non-compliance with the requirements of PFRS 15 would lead to unreliable revenue recognition, and thus, financial statements would not be faithfully represented. This may lead to wrong economic decision-making.

Three research gaps were revealed between AI and accounting. The first gap concerned the lack of studies testing the effectiveness of AI across the five steps of the revenue recognition model. The second gap was territorial, meaning that most inquiries came from North American or European samples, leaving Philippine-specific insights underdeveloped. Finally, the third gap concerned linkage: there were no technological variables linking AI to financial reporting accuracy.

Theoretical Framework

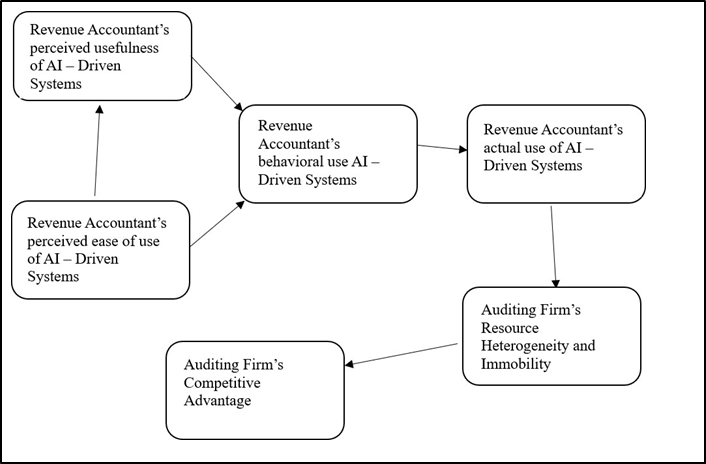

The study was based on two viewpoints: the Technology Acceptance Model (TAM) and the Resource– Based View (RBV). Figure 1 illustrates the fusion between TAM and RBV in relation to this study. The Technology Acceptance Model (TAM) is a seminal framework for explaining and predicting user adoption of new technologies. TAM theorizes that users’ behavioral intentions to use a system are chiefly determined by their perceptions of the system’s usefulness and ease of use (Lee et al., 2025). TAM identifies four factors that influence acceptance of new technology. The first factor is Perceived Usefulness (PU), which is the degree to which a person believes that using the technology will enhance their job performance or productivity (Lee et al., 2025). In the context of this study, Certified Public Accountants (CPAs) see that AI-driven systems may provide benefits (such as reducing manual transaction recording) in implementing PFRS 15. The second factor is Perceived Ease of Use (PEOU), which is the degree to which a person believes that using the technology will be effort-free (Lee et al., 2025). In the context of this study, CPAs see that AI-driven systems are easy to use, which reduces their resistance to using them. The third factor is Behavioral Intention to Use (BI), which is a user’s intention to use the technology that is directly influenced by PU and PEOU. In this study, when CPAs find the AI-driven system useful, they form a favorable intention to incorporate it into their workflow (Lee et al., 2025). The fourth factor is Actual System Use, which is the application of the technology in actual work. In the context of this study, CPAs regularly use an AI-driven system for revenue recognition transactions (i.e., the application of the five–step model) as part of their financial reporting process (Lee et al., 2025).

Figure 1: Application of TAM and RBV to Revenue Accountant’s Perception of AI – Driven Systems

Existing studies have shown that applying TAM to accounting and AI confirms their importance. For example, a study on accounting information systems found that both perceived usefulness and ease of use had significant positive effects on the intention to adopt new technology (Wicaksono et al., 2023). In another study, it was confirmed that TAM’s factors influence the acceptance of AI tools in the accounting profession (Kayser & Telukdarie, 2024). TAM allows external factors, such as training and company support, to indirectly affect the adoption of an AI-driven system. Providing such support to CPAs may increase PU or PEOU, thereby increasing system adoption.

RBV is a concept of strategic management which suggests that a firm’s sustainable competitive advantage is derived from its unique resources and capabilities that are valuable, rare, inimitable, and organized (often abbreviated as the VRIO characteristics) (Chen et al., 2022). In the context of the study, an auditing firm may gain competitive advantage over other firms if it has an AI-driven system that is unique and cannot be easily acquired or copied by other firms (Chen et al., 2022). The effective use of AI tools in validating financial data, conducting predictive analytics, and performing risk assessments reflects not just tool adoption but the firm’s ability to transform such usage into unique organizational competencies. Firms that excel in this transformation gain a competitive edge in ensuring financial reporting accuracy and compliance, which are central to regulatory and client trust. If an AI-driven system provides superior functions in financial reporting (e.g., automatically parsing complex contracts, ensuring revenue is recognized according to the standard’s five-step model, and flagging inconsistencies or errors), it creates value for an auditing firm. This value manifests in improved financial reporting accuracy and reliability, more efficient compliance processes, and reduced risk of misstatement or regulatory non-compliance. In addition, auditing firms must have other functions (e.g., data management, trained personnel, and AI integration into workflows) to complement their AI-Driven system adoption. An AI-driven revenue recognition system becomes strategically meaningful only if an audit firm can absorb and utilize it. By examining the research problem through TAM and RBV, the researcher gains insight into both the human and organizational factors that determine the success of AI implementations in revenue recognition.

Conceptual Framework

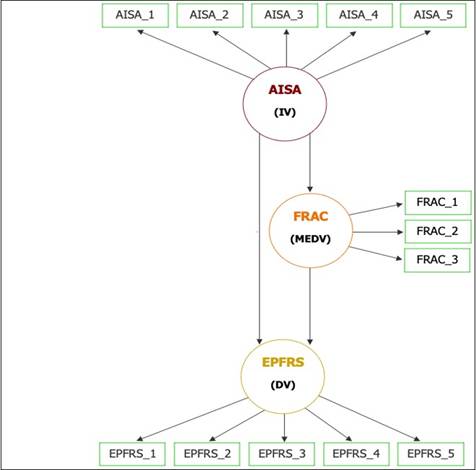

A conceptual framework comprises key concepts, variables, relationships, and assumptions that guide the academic inquiry. It establishes the theoretical foundations and provides a lens through which researchers can analyze and interpret data (Singh, 2025). It is designed to investigate how the adoption of AI-driven systems affects the implementation effectiveness of revenue recognition under PFRS 15. The framework involves three main variables, namely, AI System Adoption (AISA) as the independent variable, Financial Reporting Accuracy and Compliance (FRAC) as the mediating variable, and Effectiveness of PFRS 15 Implementation (EPFRS) as the dependent variable. Figure 1 illustrates the framework and the relationships among the variables, while Table 1 summarizes the sub-variables per independent variable, mediating variable, and dependent variable. As shown in the model, the researcher hypothesizes that AISA has positive direct effects on both FRAC and EPFRS. This means that increasing AI adoption should improve reporting accuracy and compliance, and boost the execution of the five-step process. This is consistent with evidence that AI-powered accounting improves audit quality and report reliability. For example, Hasan (2021) found that introducing AI into auditing could enhance the reliability of financial reports, increase efficiency, and optimize auditors’ processes. The researcher further hypothesizes that FRAC is the reason why AISA has a positive effect on EPFRS.

Figure 2: Conceptual Framework of Evaluating the Utilization of AI – Driven Systems in Implementing PFRS 15 on Revenue Recognition

Table 1: Summary of Variables

| Independent Variable (IV) = AI System Adoption (AISA) | |

| Data Code | Sub-Variable |

| AISA_1 | Contract Identification |

| AISA_2 | Performance Allocation |

| AISA_3 | Transaction Price Determination |

| AISA_4 | Allocation |

| AISA_5 | Revenue Recognition |

| Dependent Variable (DV) = Effectiveness of PFRS 15 Implementation (EPFRS) | |

| Data Code | Sub-Variable |

| EPFRS_1 | Automating Contract Analysis |

| EPFRS _2 | Identifying Performance Obligations |

| EPFRS _3 | Pricing Optimization |

| EPFRS _4 | Allocation Accuracy |

| EPFRS _5 | Compliance Monitoring |

| Mediating Variable (MEDV) = Financial Reporting Accuracy and Compliance (FRAC) | |

| Data Code | Sub-Variable |

| FRAC_1 | AI-driven Data Validation |

| FRAC _2 | Predictive Analytics |

| FRAC _3 | Risk Assessment |

This study evaluates the use of AI-driven systems in implementing PFRS 15 by examining how Revenue Accountants (CPAs handling revenue transactions) in the Philippines perceive AISA’s specific impact on each step of the five-step revenue recognition model: contract identification, performance obligations, transaction price determination, allocation, and revenue recognition. The study highlights AISA’s perceived effectiveness in automating contract analysis, identifying performance obligations, optimizing pricing, ensuring allocation accuracy, and monitoring compliance at each stage. Additionally, it investigates how AI-driven tools impact adherence to FRAC under PFRS 15, focusing on data validation,

predictive analytics, and risk assessment. Finally, the study seeks to provide insights into AISA’s influence on revenue recognition.

Methodology

The purpose of this study is to evaluate the implementation of AI-driven systems for revenue recognition under PFRS 15. The study employed a quantitative approach, which was deemed appropriate as the study seeks to gather structured, numerical data on hidden variables, namely AISA, EPFRS, and FRAC, by using standardized survey instruments. The collected data were subjected to advanced statistical modeling using Partial Least Squares Structural Equation Modeling (PLS-SEM), which is appropriate for analyzing complex relationships among variables, particularly for prediction and theory development (Hair et al., 2021). The study aimed to assess naturally occurring perceptions and practices among Revenue Accountants and to observe and model these relationships in a real-world setting, adhering to the principles of observational research (Babbie, 2020). Using PLS-SEM, the study sought to elucidate the direct and indirect relationships among AISA, EPFRS, and FRAC, and whether EPFRS and FRAC are the reasons AISA exists.

The study was conducted among two of the “Big Four” auditing firms in the Philippines, namely, Deloitte Philippines (Navarro, Amper & Co.) and PricewaterhouseCoopers Philippines (Isla Lipana & Co.), and Moore Philippines (Roxas Tabamo and Co.), a Mid-Tier auditing firm. Table 2 presents the population of Revenue Accountants per auditing firm, while Table 3 presents the sample size and the actual respondents per auditing firm. The number of Revenue Accountants per auditing firm was obtained through inquiry with each firm’s Human Resources Department. In computing the sample size, the study used Cochran’s formula with a 90% confidence level and a 10% margin of error. Because the population is less than 10,000, the study used the Finite Population Correction (FPC) to adjust the sample size. Stratum weights were also computed to determine the proportion of each sample size within each auditing firm relative to the entire sample.

Table 2: Respondent’s Population Distribution

| Accounting/Auditing Firm | Revenue Accountants |

| Moore Philippines | 115 |

| Navarro, Amper & Co. (Deloitte) | 400 |

| Isla Lipana & Co. (PwC) | 750 |

| TOTAL N | 1,265 |

Table 3: Summary of the Sample Size Determination and Allocation to the Respondent Auditing Firms

| Accounting/Auditing Firm | Stratum Weights (𝑾𝒉) | Sample Size (𝒏𝒉) | Actual Respondents |

| Moore Philippines | 9.38% | 6 | 6 |

| Navarro, Amper & Co. (Deloitte) | 31.25% | 20 | 17 |

| Isla Lipana & Co. (PWC) | 59.37% | 38 | 19 |

| TOTAL 𝒏 | 100.00% | 64 | 42 |

To efficiently collect data, the researcher used a self-constructed questionnaire composed of 13 items through Google Forms. A secure hyperlink or QR code was distributed to the managing partners or department heads of participating auditing firms, who disseminated it exclusively to their Revenue Accountants. All responses were summarized in a linked Google Sheet and were forwarded to the statistician for analysis. To interpret the responses meaningfully, the following four-point Likert scales were used (Table 4).

Table 4: Four-Point Likert Scale Interpretations

| SOP 1: Perceived Extent of AI System Adoption in the Implementation of the PFRS 15 Five-Step Revenue Recognition Model | |

| Scale | Interpretation |

| 4 | Fully Adopted |

| 3 | Mostly Adopted |

| 2 | Minimally Adopted |

| 1 | Not Adopted at all |

| SOP 2: Perceived Effectiveness of AI System Adoption in Executing the PFRS 15 Revenue Recognition Process | |

| Scale | Interpretation |

| 4 | Very Effective |

| 3 | Moderately Effective |

| 2 | Slightly Effective |

| 1 | Not Effective at all |

| SOP 3: Perceived Level of Adherence to Financial Reporting Accuracy and Compliance under PFRS 15 as Supported by AI-Enabled Processes | |

| Scale | Interpretation |

| 4 | Fully Adhered |

| 3 | Mostly Adhered |

| 2 | Partially Adhered |

| 1 | Not Adhered at all |

To determine the perceived extent of AISA among Revenue Accountants, the perceived effectiveness of AISA in executing PFRS 15, and the perceived level of adherence to FRAC as reinforced by AISA, the researcher computed the mean, variance, and standard deviation of the responses. This was important for identifying trends, the central tendency, and the dispersion of responses. Table 5 presents the verbal interpretations that were relevant to the data analysis in this study.

Table 5: Four-Point Likert Scale Verbal Interpretations

| SOP 1: Perceived Extent of AI System Adoption in the Implementation of the PFRS 15 Five-Step Revenue Recognition Model | |

| Mean | Verbal Interpretation (VI) |

| 3.25 – 4.00 | Very High Extent (VHEX) |

| 2.50 – 3.24 | High Extent (HEX) |

| 1.75 – 2.49 | Low Extent (LEX) |

| 1.00 – 1.74 | Very Low Extent (VLEX) |

| SOP 2: Perceived Effectiveness of AI System Adoption in Executing the PFRS 15 Revenue Recognition Process | |

| Mean | Verbal Interpretation (VI) |

| 3.25 – 4.00 | Very High Effectiveness (VHEF) |

| 2.50 – 3.24 | High Effectiveness (HEF) |

| 1.75 – 2.49 | Low Effectiveness (LEF) |

| 1.00 – 1.74 | Very Low Effectiveness (VLEF) |

| SOP 3: Perceived Level of Adherence to Financial Reporting Accuracy and Compliance under PFRS 15 as Supported by AI-Enabled Processes | |

| Mean | Verbal Interpretation (VI) |

| 3.25 – 4.00 | Very High Adherence (VHA) |

| 2.50 – 3.24 | High Adherence (HA) |

| 1.75 – 2.49 | Low Adherence (LA) |

| 1.00 – 1.74 | Very Low Adherence (VA) |

To draw insights from AISA and Revenue Recognition, the study employed PLS-SEM to model the relationships among AISA, FRAC, and EPFRS. In using PLS-SEM, convergent and discriminant validity were established. Convergent validity was assessed by computing the Average Variance Extracted (AVE), and if AVE ≥ 0.50, the variable explains at least half of the indicator variance (Venturini & Mehmetoglu, 2019). The AVE of AISA and EPFRS was 0.90 and 0.815, respectively. An AVE of this magnitude indicated that AISA’s indicators accounted for a very high proportion of variance in their underlying variable, suggesting that the items were highly representative of AI adoption behaviors in the PFRS 15 context. The AVE of EPFRS suggested that respondents consistently recognized the effectiveness of AI-driven processes across the five procedural steps of PFRS 15, resulting in high shared variance among indicators. Discriminant validity is used to explain that each variable is explained by its unique variance. To assess discriminant validity, the heterotrait-monotrait (HTMT) ratio of correlations was used. HTMT ratio is the ratio of the average correlations across constructs (heterotrait–heteromethod correlations) to the average correlations within the same construct (monotrait–heteromethod correlations) (Henseler et al., 2015). The HTMT value close to 1 suggests that the variables are not empirically distinct, whereas a lower HTMT indicates they differ. Two cutoffs are available. A value of 0.85 is recommended when constructs are expected to be conceptually distinct, whereas a more lenient cutoff of 0.90 may be used when constructs are very similar. Discriminant validity is achieved when the HTMT ratio of a variable is below

0.85 or below 0.90 (for similar variables). The study adopted the 0.90 cutoff as AISA and EPFRS are theoretically related based on TAM and RBV. The association between AISA and EPFRS yielded an HTMT ratio of 0.858, below the 0.90 cutoff. This indicated acceptable discriminant validity, meaning that while the constructs were meaningfully correlated, they did not measure the same underlying concept. The researcher estimated the following paths (AISA→FRAC, AISA→EPFRS, and FRAC→EPFRS) using PLS-SEM. To assess the model’s explanatory power, the coefficient of determination (R²) and adjusted coefficient of determination (AIC) were computed. R² ranges from 0 to 1, with higher values indicating greater explained variance. Common guidelines classify R² values as 0.26 (substantial), 0.13 (moderate), and 0.02 (weak) (Cohen, 1988). R² values were 0.793 and 0.767, respectively. This suggested that almost 80% of the variance in EPFRS was explained by the model’s predictors. Effect size and predictive relevance were also reported. Effect size calculates how much a dependent variable’s R² changes when a specific independent variable is omitted from the model. Cohen (1988) suggests f² values of 0.02, 0.15, and 0.35 correspond to small, medium, and large effects, respectively. The computed f² was 0.421, exceeding the threshold of 0.35, indicating a large effect size. This means that removing the key predictor would significantly reduce the model’s explanatory capability, highlighting the substantial contribution of AI system adoption and compliance-related accuracy to improving PFRS 15 implementation outcomes. Predictive relevance is a measure of the association between an independent and a dependent variable. If

> 0, then the model has good predictive power. The computed Q² value of 0.355 confirmed that the model has strong predictive relevance. Variance Inflation Factors (VIF) are computed. VIF is necessary to determine if each variable in the model is not redundant and contributes uniquely to the model. VIF < 5 indicates no redundancy of variables. The VIF score of 0.343 indicated that each variable contributed uniquely to the model, without redundancy. Finally, bootstrapping is done to produce path coefficients and other necessary parameters (Leguina, 2015). Resampling is done from the original sample, permitting strong statistical inference for small samples or complex data. The study used 5,000 resamples.

This study strictly adhered to ethical standards governing research involving human participants. All procedures were carefully designed to protect respondents’ rights, privacy, and dignity throughout data collection and analysis. The Google Form included an informed consent statement outlining the study’s purpose, the voluntary nature of participation, the estimated time commitment, assurances of confidentiality, and data protection. Respondents were informed that they had the right to withdraw at any time or to skip any item they were not comfortable answering. Respondent’s personal information, such as names and email addresses, was not collected. All responses were stored in a secure Google Drive folder

accessible only to the researcher and the assigned statistician. The data will be retained for academic purposes only and will be permanently deleted one year after the completion of the study. Should institutional review be required, full documentation is available for submission.

Results and Discussion

The following tables present the statistical analysis of data collected from the respondents and the interpretation of these data. The results presented in Tables 6, 7 and 8 applied descriptive statistics while the results in Tables 9 and 10 applied PLS-SEM with bootstrapping. Table 6 summarizes the current extent of AI adoption in using PFRS 15. Tables 7 and 8 summarize respondents’ perception on the usefulness of AI in applying PFRS 15 and if respondents perceive that FRAC is the reason why AI is used in applying PFRS 15. Tables 9 and 10 present the direct and indirect path results between AISA, FRAC, and EPFRS.

Table 6: Perceived Extent of AI System Adoption (AISA) among Revenue Accountants in the Philippines when implementing the PFRS 15 Five-Step Revenue-Recognition Model

| Research Indicators | Mean | SD | Variance | VI |

| 1. To what extent is AI integrated in identifying and verifying contracts with customers under PFRS 15? | 2.36 | 0.850 | 0.723 | LEX |

| 2. To what extent is AI adopted in identifying distinct performance obligations within contracts? | 2.26 | 0.828 | 0.686 | LEX |

| 3. To what extent is AI utilized in determining the transaction price based on contractual terms and relevant data inputs? | 2.43 | 1.016 | 1.031 | LEX |

| 4. To what extent is AI implemented in allocating the transaction price across identified performance obligations? | 2.38 | 0.936 | 0.876 | LEX |

| 5. To what extent is AI employed in recognizing revenue as performance obligations are satisfied under PFRS 15? | 2.29 | 0.944 | 0.892 | LEX |

| Overall Results | 2.34 | 0.915 | 0.842 | LEX |

In Table 6, the computed mean of 2.34, with a standard deviation of 0.915 and a variance of 0.842, indicated a Low Extent (LEX) of AI System Adoption among Revenue Accountants across the five PFRS 15 steps. This suggested that while AI tools may be present in selected aspects of revenue accounting, they were neither consistently applied nor deeply embedded in revenue recognition processes. The standard deviations (0.828–1.016) and variances (0.686–1.031) indicated moderate variability in responses, suggesting that although AISA was generally low, differences across firms persist, potentially reflecting differences in technological capacity, system maturity, and workflow integration. The highest mean (M = 2.43) appeared in transaction price determination, suggesting slightly greater exposure to AI-driven analytics in price-related computations. On the other hand, the lowest (M = 2.26) was for identifying distinct performance obligations, suggesting a notable gap in AI’s ability or in firms’ willingness to automate judgment-intensive tasks related to contract disaggregation. These results indicated that AI technology has not yet achieved operational maturity in the revenue recognition workflows of most accounting and auditing firms in Metro Manila. This may be due to several factors such as high implementation cost and system-upgrade requirements (Osma, Conde & Mora, 2023), limited training and digital competence among accountants, organizational hesitation stemming from risk perception, regulatory scrutiny, and algorithm transparency concerns (Rana, Dwivedi & Akter, 2022), and the inherent complexity of PFRS 15, which demands professional judgment that AI tools may not yet fully replicate. It may be inferred that the auditing firms were still in the early stages of incorporating AI-driven tools into

their revenue recognition workflows. This limited adoption was consistent across contract identification, performance-obligation analysis, transaction-price determination, allocation, and recognition, indicating that AI had not yet been systematically embedded into the technical processes required by the standard.

Table 7: Perceived Level of Effectiveness of AI System Adoption in Each Step of the PFRS 15 Revenue Recognition Model (EPFRS)

| Research Indicators | Mean | SD | Variance | VI |

| 1. How effective is AI in automating the extraction and analysis of contract terms relevant to revenue recognition? | 2.71 | 0.835 | 0.697 | HEF |

| 2. How effective is AI in accurately identifying and classifying performance obligations in complex contractual arrangements? | 2.52 | 0.707 | 0.499 | HEF |

| 3. How effective is AI in enhancing transaction price determinations through predictive modeling or rule- based adjustments? | 2.64 | 0.759 | 0.577 | HEF |

| 4. How effective is AI in improving the accuracy of transaction price allocations to performance obligations? | 2.60 | 0.828 | 0.686 | HEF |

| 5. How effective is AI in monitoring compliance with PFRS 15’s recognition, measurement, and disclosure requirements? | 2.67 | 0.846 | 0.715 | HEF |

| Overall Results | 2.63 | 0.795 | 0.635 | HEF |

In Table 7, the computed mean score of 2.63, with a standard deviation of 0.795 and a variance of 0.635, reflected a High Effectiveness (HEF) rating of AI-driven systems in enhancing PFRS 15 compliance across its five core procedural components. This suggested that Revenue Accountants recognized AI as substantially valuable for improving revenue recognition processes. The highest mean of 2.71 pertained to AI’s effectiveness in automating contract analysis, indicating that respondents perceived AI as most helpful for extracting and reviewing contract terms relevant to PFRS 15. Conversely, the lowest mean of

2.52 indicated AI’s accuracy in identifying and classifying performance obligations, suggesting this remained a difficult aspect for AI to fully master due to the task’s interpretive and judgment-based nature. Moderate standard deviations (0.707–0.846) suggested a relatively consistent perception among respondents. While AISA was at a Low Extent, its effectiveness was perceived as high, suggesting that Revenue Accountants acknowledged the benefits across the five-step model. The pattern indicated that AI was most effective when operating on structured, data-heavy tasks—such as contract extraction, transaction price computation, and compliance monitoring—while interpretive tasks that require professional judgment—such as identifying performance obligations—still relied more heavily on human expertise. The findings point to the emphasis that AI was particularly useful for contract review, pattern recognition, and anomaly detection (Solanki & Manduva, 2024), a Rules Engine in AI for automated revenue recognition, explaining its effectiveness in allocation accuracy, compliance monitoring, and handling transactional data (Berwanger, 2025), and AI’s advantage in dynamic pricing and analytical computations (Huang & Rust, 2021 and Momin & Mishra, 2024). From the theoretical perspectives of TAM and RBV, these results implied that perceived usefulness, a major determinant of behavioral intention, was already well established, and that increasing adoption (AISA) was likely to further strengthen both financial reporting accuracy (FRAC) and overall implementation effectiveness (EPFRS).

Table 8: Perceived Level of Adherence to Financial Reporting Accuracy and Compliance (FRAC) under PFRS 15

| Research Indicators | Mean | SD | Variance | VI |

| 1. To what extent does AI contribute to accurate and real-time validation of financial data for PFRS 15 compliance? | 2.55 | 0.832 | 0.693 | HA |

| 2. To what extent does AI-supported predictive analytics improve foresight and decision-making in revenue recognition practices? | 2.67 | 0.846 | 0.715 | HA |

| 3. To what extent does AI enhance the identification and mitigation of risks related to financial reporting and PFRS 15 compliance? | 2.55 | 0.832 | 0.693 | HA |

| Overall Results | 2.59 | 0.837 | 0.700 | HA |

In Table 8, the overall mean of 2.59, with a standard deviation of 0.837 and a variance of 0.700, indicated a High Adherence (HA) to financial reporting accuracy and compliance supported by AI-driven tools. All three indicators fell within the HA range, with mean values ranging from 2.55 to 2.67, suggesting that respondents consistently perceived AI as beneficial for PFRS 15 compliance. The highest rating, 2.67, was for AI-supported predictive analytics, indicating that Revenue Accountants viewed AI’s ability to provide foresight and decision support as particularly impactful in improving revenue recognition practices. Meanwhile, the indicators related to real-time data validation (M = 2.55) and risk mitigation (M = 2.55) also received high adherence ratings, reflecting a strong belief that AI enhanced accuracy by reducing manual errors, detecting anomalies, and elevating the reliability of financial information. Variances between 0.693 and 0.715 indicated moderate variability, suggesting that most respondents shared similar perceptions of AI’s role in ensuring compliance under PFRS 15.

The high adherence levels suggest that Revenue Accountants are gradually relying on AI to validate data, identify inconsistencies, and assess compliance risks, especially given the heavy judgment and documentation required under PFRS 15. The high rating for predictive analytics implied that Revenue Accountants recognize AI’s capability to forecast potential reporting issues, enabling better preparation and mitigation strategies. These findings also hinted at a broader organizational shift toward integrating AI into quality-assurance functions, demonstrating growing trust in AI-assisted decision-making in financial reporting contexts. These findings closely reflected insights emphasized across studies by Pallathadka et al. (2023) and Huang & Rust (2021), who underscored that AI provides value to a firm through predictive analytics and enhanced decision-making. The high adherence results also confirm that AI reduces restatements, improved audit quality, and strengthened fraud detection, all key aspects of revenue recognition (Fedyk et al., 2022).

Overall, the findings demonstrated that AI significantly enhanced organizational adherence to financial reporting accuracy and compliance under PFRS 15. The consistently high scores across all indicators showed that AI-driven data validation, predictive analytics, and risk mitigation collectively improved the integrity, transparency, and reliability of revenue-related disclosures. When viewed alongside SOP 1 and SOP 2, a developing pattern becomes evident: although AI adoption (AISA) was still low, its perceived effectiveness (EPFRS) and contribution to reporting accuracy (FRAC) were both high. This triangulated result proposed that increased AISA would likely generate faithfully represented reports.

Table 9: Bootstrapped Direct Model Parameter Estimates (AISA -> EPFRS)

| Latent | Observed | Estimate | Standard Error | 95% Confidence Interval | 𝜷 | 𝑷 − 𝑽𝒂𝒍𝒖𝒆 | |

| Lower | Upper | ||||||

| AISA | AISA1 | 0.934 | 0.041 | 0.798 | 0.987 | 0.934 | < 0.00001 |

| AISA2 | 0.938 | 0.036 | 0.824 | 0.990 | 0.938 | < 0.00001 | |

| AISA3 | 0.979 | 0.023 | 0.918 | 1.014 | 0.979 | < 0.00001 | |

| AISA4 | 0.943 | 0.030 | 0.857 | 0.987 | 0.943 | < 0.00001 | |

| EPFRS | EPFRS1 | 0.839 | 0.067 | 0.649 | 0.938 | 0.839 | < 0.00001 |

| EPFRS2 | 0.940 | 0.055 | 0.769 | 1.015 | 0.940 | < 0.00001 | |

| EPFRS3 | 0.903 | 0.047 | 0.723 | 0.965 | 0.903 | < 0.00001 | |

| EPFRS4 | 0.926 | 0.060 | 0.758 | 1.013 | 0.926 | < 0.00001 | |

The PLS-SEM direct path results (Table 9) demonstrated a statistically robust and significant causal effect of AI System Adoption on the Effectiveness of PFRS 15 Implementation, with a path coefficient of β = 0.934, a narrow 95% confidence interval [0.798, 0.987], and a p-value < 0.00001. This indicated that as auditing firms increased their adoption of AI-driven systems, whether through automated contract analysis tools, machine-learning-based transaction-price algorithms, rule-based allocation engines, or compliance- monitoring software, the effectiveness of PFRS 15 implementation also increased. All indicator loadings were very strong for both AISA (0.934–0.979) and EPFRS (0.839–0.926), confirming excellent measurement reliability and stable latent-variable representation. These results showed that Revenue Accountants consistently associated higher levels of AI adoption with significant improvements in the execution of the PFRS 15 model, reinforcing the consistent pattern found where AI was already perceived as highly effective and highly compliance-enhancing. These findings implied that AI-driven tools acted as a decisive mechanism enabling Revenue Accountants to navigate the technical and judgment-intensive requirements of PFRS 15. Even though adoption remained low in practice, the extremely high coefficient suggested that when AI tools were used, they yielded meaningful improvements in accuracy, consistency, judgment support, and process efficiency. The positive direct effect of AISA on EPFRS suggests that auditing firms adopting AI may mitigate burdens in applying PFRS 15, such as contract analysis, performance-obligation identification, allocation, and disclosure, thereby reducing workload, training costs, and the risk of misapplication. The findings also supported that AI systems, such as Beagle, excel at identifying terms and enforceable rights in a contract (Solanki and Manduva, 2024). Furthermore, the findings confirmed that a Rules Engine serves as the foundational logic layer for automated revenue recognition (Berwanger, 2025) and that, when coupled with AI, the output can be enhanced through pattern recognition, predictive modeling, and anomaly detection, thereby improving the timing and accuracy of revenue recognition.

The very strong, positive, and significant effect (β = 0.934; p < 0.00001) indicates a significant positive relationship between AI adoption and the effectiveness of PFRS 15 revenue recognition steps. The findings confirmed that AISA was a powerful determinant of EPFRS. Despite limited adoption in practice, the high coefficient indicates that auditing firms that integrate AI into revenue workflows achieve substantially improved compliance, accuracy, and execution of the five-step revenue recognition model. When triangulated with the descriptive findings (i.e., Low AISA, High EPFRS, High FRAC), the PLS-SEM confirmed a consistent statistical pattern: AI improves reporting quality and standard compliance when used.

Table 10: Bootstrapped Indirect Path Model Significant Parameter Estimates

| Effect | Estimate | Standard Error | 95% Confidence Interval | 𝜷 | 𝑷 − 𝑽𝒂𝒍𝒖𝒆 | |

| Lower | Upper | |||||

| AISA12 -> FRAC1 -> EPFRS | -0.108 | 0.291 | -2.397 | -0.124 | -0.073 | < 0.050 |

| AISA12 -> FRAC2 -> EPFRS | -0.158 | 0.649 | -1.238 | -1.024 | -0.107 | < 0.010 |

| AISA22 -> FRAC2 -> EPFRS | 0.253 | 0.701 | -1.258 | -1.149 | 0.168 | < 0.050 |

| AISA52 -> FRAC1 -> EPFRS | -0.052 | 0.272 | -2.205 | -0.127 | -0.030 | < 0.050 |

Across the four significant indirect pathways presented in Table 10, the results confirmed that FRAC functioned as a statistically significant mediator between AISA and EPFRS. Although the estimates vary in magnitude and sign due to item-level nuances, all p-values fell below the 0.050 threshold, indicating that FRAC indeed accounted for a meaningful portion of AISA’s influence on PFRS 15 implementation. The indirect effects involving FRAC1 (Data Validation) showed that when AI enhanced real-time validation, anomaly detection, and accuracy checks, it indirectly supported EPFRS by reducing errors in contract processing, allocation, and disclosure. The indirect pathways involving FRAC2 (Predictive Analytics), particularly the AISA2 → FRAC2 → EPFRS effect, exerted the strongest mediating influence, confirming that AI-generated foresight, trend analysis, and predictive modeling significantly enhanced accountants’ ability to perform transaction price determinations, evaluate performance obligation fulfillment, and anticipate issues in measurement and disclosure. This aligned with the descriptive results, which showed that FRAC2 had the highest mean among the FRAC indicators. The indirect effects involving FRAC3 (Risk Identification & Mitigation) indicated that AI contributed to EPFRS by detecting compliance risks, inconsistencies, and ambiguities in revenue classification that may otherwise jeopardize adherence to PFRS 15. Even modest coefficients reflected how AI-supported risk mitigation alleviated the implementation of the PFRS 15 model by reducing misstatements and control failures. Overall, the significant indirect pathways validated that AISA’s influence on EPFRS was partially transmitted through AI’s data accuracy, predictive strength, and compliance-risk mitigation functions. These findings implied that AI further improved PFRS 15 implementations by strengthening the accuracy, analytical foresight, and risk management functions required to correctly apply PFRS 15. AI-driven data validation (FRAC1) ensured that contract data, transaction-price inputs, and allocation bases were accurate. AI-supported predictive analytics (FRAC2) empowered Revenue Accountants with decision-support insights, enabling better forecasting of revenue trends, identification of fulfillment timing, and allocation planning. AI-based risk mitigation (FRAC3) prevented compliance errors that commonly arise in disclosures and measurements. Collectively, these mechanisms formed a strong mediating layer, confirming that AISA improves and enhances the application of PFRS 15.

Because AISA significantly predicted FRAC across its indicators, the findings confirmed that AI adoption significantly improved accuracy, predictive analytics, and risk mitigation. Since FRAC significantly predicted EPFRS across the indirect pathways, the findings verified a significant positive relationship between FRAC and EPFRS (i.e., improvements in FRAC were associated with higher EPFRS). The mediation analysis confirmed that FRAC served as a significant and meaningful pathway through which AI adoption enhanced the effectiveness of PFRS 15 revenue recognition processes.

Conclusions and Recommendations

The limited extent of AISA adoption across the five-step revenue recognition model in PFRS 15 confirmed that auditing firms have not yet fully implemented AI-driven systems for transactions involving revenue recognition. The status may be attributed to factors such as high maintenance cost, technological unemployment, resistance by Revenue Accountants, technological breakdowns and failures, and

nontransparency. On the other hand, Revenue Accountants perceived that AI is highly effective at each step of the revenue recognition model. They showed assurance that AI-driven systems were beneficial in the implementation of PFRS 15. Because Revenue Accountants perceived that AI is highly effective in applying PFRS 15, they also believed that AI has high compliance with financial reporting requirements. They believed that applying AI enhances the reporting requirements of PFRS 15, leading to faithful representation of revenue transactions, improved forecasting of revenue data to make better economic decisions in the future, reduced manual errors, and detection of irregularities in PFRS 15 applications. These indirect paths (AISA → FRAC → EPFRS) indicate that data validation, predictive analytics, and risk mitigation corroborate the significant positive relationship between AISA and EPFRS. Thus, respondents perceived AI’s usefulness and viewed it as a strategic resource that could give an audit firm a competitive advantage.

The researcher recommended that auditing firms invest in AI-driven systems specifically designed for revenue recognition under PFRS 15. Such a system may include features such as Beagle for contract identification and a Rules Engine for measurement and compliance with PFRS 15. Auditing firms may host seminars showing the capability of AI in applying PFRS 15 and can present a cost-benefit analysis of incorporating this system in the current workflow. This move by auditing firms should have the support of professional bodies (e.g., the Board of Accountancy, and the Philippine Institute of Certified Public Accountants) to boost AI’s legitimacy and credibility in the accountancy profession. Finally, for future researchers, this research may serve as a stepping stone to further investigate whether the size of an auditing firm (e.g., revenue volume or number of CPAs employed) may affect AI adoption under PFRS

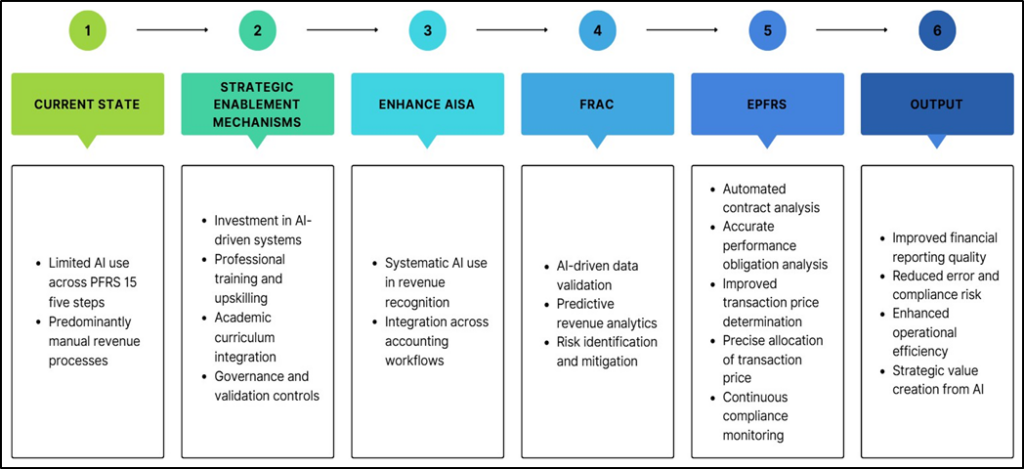

15. The researcher further suggests an output model that may aid in developing an AI system specifically designed for PFRS 15 (Figure 2).

Figure 3: AI-Enabled PFRS 15 Implementation Enhancement Model

Findings revealed that the implementation of PFRS 15 mainly depended on manual procedures. To bridge this gap, the model introduces strategic enablement mechanisms as a necessary transitional component. These mechanisms include organizational investment in AI-driven systems, professional training and upskilling of revenue accountants, integration of AI-related competencies into academic curricula, and the establishment of governance and validation controls. Following strategic enablement, the model advances to enhanced AI system adoption, wherein AI tools are systematically integrated into accounting workflows and revenue recognition processes. This stage reflects a shift from limited or ad hoc use to more consistent, structured AI applications. Central to the framework is Financial Reporting Accuracy and Compliance (FRAC), which operates as a mediating mechanism. Consistent with the study’s results, improved AI

adoption enhances financial reporting accuracy through AI-driven data validation, predictive analytics, and risk assessment. This translates to strengthened accuracy and compliance with PFRS 15. The model then leads to the Effectiveness of PFRS 15 Implementation, reflecting respondents’ high perceived effectiveness of AI when it is used. The model demonstrates that AI-driven systems contribute to effective PFRS 15 implementations not solely through automation, but also by enhancing accuracy, compliance, and process reliability.

Acknowledgment

The researcher would like to express his gratitude to his thesis adviser, Dr. Robert Y. Co, whose expertise was invaluable during the thesis. Sincere thanks to his statistician, Edgard Ivan C. Gonzaga, for assisting with the statistical data. The researcher would also like to thank his thesis professor and the College Dean of La Consolacion College Manila (LCCM), Dr. Maximo Muldong, for guidance in structuring this thesis. The researcher thanks personnel from auditing firms, Jewel Marie Villanueva of PwC Philippines, Errol Pielago, HR Senior Manager of Deloitte Philippines, Atty. Tristan Lopez, CPA of Deloitte Philippines, Madelyn Laurel, Human Resource Manager of Moore Philippines, Lujer Danao, CPA, and Rose Anne Valix, CPA, Tax Services and Business Services Outsourcing Partner, of Moore Philippines, for their assistance in disseminating the survey to the respondents. Similarly, the researcher would like to thank Malou Jackob, LCCM Graduate School Secretary, Assistant Professor Carl Francis T. Castro, Dean of LCCM Graduate School, Dr. Ronald M. Pastrana, Vice President for Academics, LCCM, Dr. Cayetano Nicolas, and Dr. Luz Dasmariñas for their academic support and teachings during his MBA Program. Lastly, the researcher wants to acknowledge his family for their love and encouragement. He would like to thank his wife, Marie F. Valix, and his children, Zoe Marie F. Valix and Nia Anneliese F. Valix, for their patience, understanding, and inspiration. He would like to recognize also his parents, Atty. Conrado T. Valix, CPA, and Susan M Valix, CPA, and his brother, Ronald M. Valix, CPA, for believing in his capabilities.

References

- Ajayi-Nifise, A. O., Odeyemi, O., Mhlongo, N. Z., Ibeh, C. V., Elufioye, O. A., & Awonuga, K. F. (2024). The future of accounting: Predictions on automation and AI integration. World journal of advanced research and reviews, 21(2), 399-407.

- Alhazmi, A., Islam, S. M. N., & Prokofieva, M. (2022). The impact of artificial intelligence adoption on the quality of financial reports on the Saudi Stock Exchange. International Journal of Financial Studies, 13(1), 21. https://doi.org/10.3390/ijfs13010021

- Asker, J., Fershtman, C., & Pakes, A. (2021). Artificial intelligence and pricing: The impact of algorithm design (No. w28535). National Bureau of Economic Research.

- Babbie, E. (2020). The practice of social research (15th ed.). Cengage Learning.

- Beard, J. (2024). Simple sample size calculations for cross-sectional studies. South Sudan Medical Journal, 17(4), 213–216. https://dx.doi.org/10.4314/ssmj.v17i4.12

- Berwanger, J. (2025). Automated revenue recognition: The 2024 guide. HubiFi.

- Canhoto, A. I., & Clear, F. (2020). Artificial intelligence and machine learning as business tools: A framework for diagnosing value destruction potential. Business Horizons, 63(2), 183-193.

- Chen, D., Esperança, J. P., & Wang, S. (2022). The impact of artificial intelligence on firm performance: An application of the resource-based view to e-commerce firms. Frontiers in Psychology, 13, 884830. https://doi.org/10.3389/fpsyg.2022.884830

- Chin, W. W. (2010). How to write up and report PLS analyses. In V. E. Vinzi, W. W. Chin, J. Henseler, & H. Wang (Eds.), Handbook of partial least squares: Concepts, methods and applications (pp. 655–690). Springer. https://doi.org/10.1007/978-3-540-32827-8_29

- Davis, F. D. (1989). Perceived usefulness, perceived ease of use, and user acceptance of information technology. MIS Quarterly, 13(3), 319–340. https://doi.org/10.2307/249008

- Dela Cruz, M. (2025, January 1). Facts 101: What to know about the Big Four accounting firms.

D&V Philippines | Finance and Accounting Outsourcing Company https://www.dvphilippines.com/blog/facts-101-what-to-know-about-the-big-four-accounting-firms - Deloitte Philippines. (n.d.). About Deloitte Philippines. https://www.deloitte.com/southeast- asia/en/about/philippines.html

- Fedyk, A., Hodson, J., Khimich, N., & Fedyk, T. (2022). Is artificial intelligence improving the audit process. Review of Accounting Studies, 27(3), 938-985.

- Google search. (n.d.). Forbes. https://www.forbes.com/advisor/business/software/ai-in- business/#methodology_section

- Hair, J. F., Hult, G. T. M., Ringle, C. M., & Sarstedt, M. (2021). A primer on partial least squares structural equation modeling (PLS-SEM) (3rd ed.). SAGE Publications.

- Hasan, A. R. (2021). Artificial Intelligence (AI) in accounting & auditing: A Literature review. Open Journal of Business and Management, 10(1), 440-465.

- Hasan, M. K., & Kumar, L. (2021). Determining adequate sample size for social survey research.

Journal of Bangladesh Agricultural University, 19(2), 168–177. https://doi.org/10.3329/jbau.v22i2.74547 - Henseler, J., Ringle, C. M., & Sarstedt, M. (2016). Testing measurement invariance of composites using partial least squares. International Marketing Review, 33(3), 405–431. https://doi.org/10.1108/IMR-09-2014-0304

- Hońko, S., & Hendryk, M. (2024). The Role of AI in Accounting: Insights From Practitioners. European Research Studies Journal, 27(2), 989-1003.

- How Gen AI and analytical AI differ — and when to use each. (2024, December 13). Harvard Business Review. https://hbr.org/2024/12/how-gen-ai-and-analytical-ai-differ-and-when-to-use-each

- How many companies use AI? (New data). (2023, July 24). Exploding Topics. https://explodingtopics.com/blog/companies-using-ai

- Huang, M. H., & Rust, R. T. (2021). A strategic framework for artificial intelligence in marketing. Journal of the academy of marketing science, 49, 30-50.

- IFRS. (2018). IFRS 15: Revenue from Contracts with Customers

- Kayser, K., & Telukdarie, A. (2024). Literature review: Artificial intelligence adoption within the accounting profession applying the Technology Acceptance Model. In Remodeling Businesses for Sustainable Development (pp. 217–231). Springer. https://doi.org/10.1007/978-3-031-46177-4_12

- KPMG International. (2024). AI in financial reporting and audit: Navigating the new era.

- Kvam, P. H., Vidakovic, B., & Kim, J. (2022). Nonparametric

- Lee, A. T., Ramasamy, R. K., & Subbarao, A. (2025). Understanding psychosocial barriers to healthcare technology adoption: A review of TAM and UTAUT frameworks. Healthcare, 13(3), 250. https://doi.org/10.3390/healthcare13030250

- Lee, W. J., & Choi, S. U. (2024). The effect of the new revenue recognition principle (IFRS 15) on financial statement comparability: Evidence from Korea. Journal of International Accounting Auditing and Taxation, 54, 100601. https://doi.org/10.1016/j.intaccaudtax.2024.100601

- Leguina, A. (2015). A primer on partial least squares structural equation modeling (PLS-SEM). International Journal of Research & Method in Education, 38(2), 220–221. https://doi.org/10.1080/1743727x.2015.1005806

- Ma, G., & Li, B. (2024). Leveraging AI to decipher how supply contracts map to revenues. SSRN.

- Mae, S. (2023, April 25). The “Big 4” top accounting firms in the Philippines. Business News Philippines. https://www.businessnews.com.ph/accounting-firm-philippines-20230423/

- Manduva, V. C. (2024). Implications for the Future and Their Present-Day Use of Artificial Intelligence. International Journal of Modern Computing, 7(1), 72-91.

- Mann, H. B. (2021). Mathematical statistics (3rd ed.). Dover Publications.

- Manuel, S., Molina, D., Palattao, C., Romero, C., & Turaray, J. (2019). Issues on the new revenue recognition standard (PFRS 15) by contractors in Cagayan.

- Maslak, O. I., Maslak, M. V., Grishko, N. Y., Hlazunova, O. O., Pererva, P. G., & Yakovenko, Y. Y. (2021, September). Artificial intelligence as a key driver of business operations transformation in the conditions of the digital economy. In 2021 IEEE International Conference on Modern Electrical and Energy Systems (MEES) (pp. 1-5). IEEE.

- Méndez-Suárez, M. (2021). Marketing mix modeling using PLS-SEM, bootstrapping the model coefficients. Mathematics, 9(15), 1832. https://doi.org/10.3390/math9151832

- Momin, U., & Mishra, P. (2024). E-commerce management and ai based dynamic pricing revenue optimization strategies. Migration Letters, 21(S4), 168-177.

- Moore, D. S., McCabe, G. P., & Craig, B. A. (2020). Introduction to the practice of statistics (10th ed.). W. H. Freeman.

- Moore, Roxas, Tabamo & Co. (n.d.) About Moore. https://www.roxastabamo.com/about/about- moore

- Moran, L. (2023). Revenue recognition in the age of AI. Trullion. https://trullion.com/blog/revenue- recognition-in-the-age-of-ai/?utm_source=chatgpt.com

- Moridu, I. (2023). The impact of financial statement quality on investment decision-making: A descriptive study of the banking sector in West Java. The ES Accounting and Finance, 1(3), 169– 175.

- Mouka, M. (2025). The real AI divide in accounting is between the fearful and the fearless. Accountancy Age.

- Munoko, I., Brown-Liburd, H. L., & Vasarhelyi, M. (2020). The ethical implications of using artificial intelligence in auditing. Journal of business ethics, 167(2), 209-234.

- Napier, C. J., & Stadler, C. (2020). The real effects of a new accounting standard: the case of IFRS 15 Revenue from Contracts with Customers. Accounting and Business Research, 50(5), 474-503.

- Osma, B. G., Gomez-Conde, J., & Mora, A. (2023, November). Intended and unintended consequences of IFRS 15 adoption.

- Pallathadka, H., Ramirez-Asis, E. H., Loli-Poma, T. P., Kaliyaperumal, K., Ventayen, R. J. M., & Naved, M. (2023). Applications of artificial intelligence in business management, e-commerce and finance. Materials Today: Proceedings, 80, 2610-2613.

- Perneger, T. V., Courvoisier, D. S., Hudelson, P. M., & Gayet-Ageron, A. (2015). Sample size for pre-tests of questionnaires. Quality of Life Research, 24(1), 147–151. https://doi.org/10.1007/s11136-014-0752-2

- PwC. (2024). Generative AI reshapes financial landscape. PwC. https://www.pwc.com/ph/en/tax/tax- publications/taxwise-or-otherwise/2024/generative-ai-reshapes-financial-landscape.html

- PwC Philippines. (n.d.). About Us. https://www.pwc.com/ph/en/about-us.html

- Rana, N. P., Chatterjee, S., Dwivedi, Y. K., & Akter, S. (2022). Understanding dark side of artificial intelligence (AI) integrated business analytics: assessing firm’s operational inefficiency and competitiveness. European Journal of Information Systems, 31(3), 364-387.

- Singh, S. (2025, April). What is a Conceptual Framework and How to Make It (with Examples)

Researcher.Life. https://researcher.life/blog/article/what-is-a-conceptual-framework-and-how-to- make-it-with-examples - Solanki, K. Artificial Intelligence in Contract Law. Journal of Legal Research and Juridical Sciences,

2(3). statistics with applications to science and engineering (2nd ed.). Wiley. - The state of AI in early 2024: Gen AI adoption spikes and starts to generate value. (2024, May 30). McKinsey & Company. https://www.mckinsey.com/capabilities/quantumblack/our-insights/the-state- of-ai#/

- Thomson Reuters (Tax & Accounting). (2024). How do different accounting firms use AI?

- Venkatesh, V., & Davis, F. D. (2000). A theoretical extension of the Technology Acceptance Model: Four longitudinal field studies. Management Science, 46(2), 186–204. https://doi.org/10.1287/mnsc.46.2.186.11926

- Venturini, S., & Mehmetoglu, M. (2019). plssem: A Stata Package for Structural Equation Modeling with Partial Least Squares. Journal of Statistical Software, 88(8). https://doi.org/10.18637/jss.v088.i08

- Weiss, N. A. (2021). Introductory statistics (10th ed.). Pearson.

- Wicaksono, A. R., Maulina, E., Rizal, M., & Purnomo, M. (2023). Technology Acceptance Model (TAM): Applications in accounting systems. Journal of Law and Sustainable Development, 11(5), e0547. https://doi.org/10.55908/sdgs.v11i5.547